18 May 2022#WeeklyWatch

Private Banking: protecting savings from inflation

The specter of inflation that risks eroding savings. How Private Banking can offer asset protection.

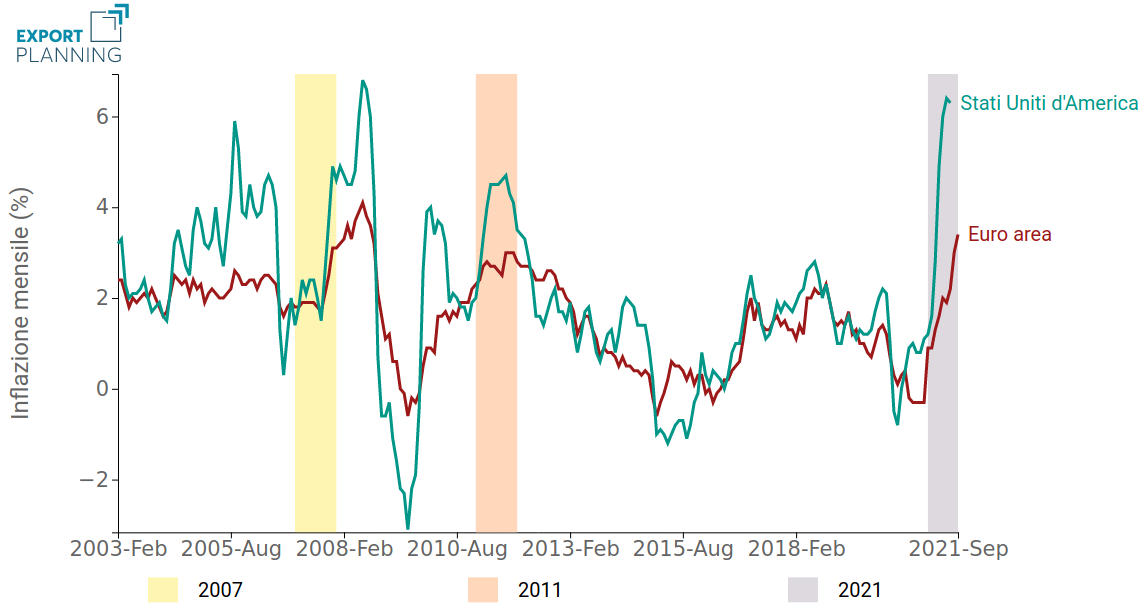

About 6% on an annual basis. This is the level reached in Italy in April by the inflation rate, according to the latest official data published by Istat.

This is a small slowdown compared to March (when there was a peak of 6.5%) but, apart from the monthly fluctuations, there is no doubt that consumer prices have returned to growth at a pace not seen since. 1991, that is, for more than 30 years now.

Which, in addition to being bad news for those who want to keep the daily expense account under control, represents a threat that should certainly not be overlooked for those who have financial capital.

(Fonte ExportPlanning.com)

Inflation and the erosion of savings

In fact, every year, the increase in prices has an erosive action on savings which, if not properly invested and made to bear fruit, inevitably lose their purchasing power.

Of course, today it is still too early to say whether we are back in an inflationary spiral like in the 80s and 90s of the last century or if it is just a transitory phenomenon, mostly linked to the recent increases in energy prices, after the outbreak of war in Ukraine.

While waiting to understand which scenario will open up, perhaps it is better not to alarm too much, remaining however aware that, if inflation increases, savers must indeed be on their guard.

If by hypothesis the average increase in prices were 4-5% for another year, for example, a sum of 100 thousand euros owned today will be worth the equivalent of today's 94-95 thousand euros in 2023.

Click here to calculate your inflation level with the tool made available by the ECB

/original/historical-inflation-rate-by-year-2022-05-17-macrotrends+%281%29.png)

Inflazione dal 1990 (Fonte MacroTrends.net)

The only possible way: to protect savings

This scenario will occur, of course, only if the wealth is left “standing still”, that is, used in non-interest bearing instruments such as current accounts. Therefore, in order to stem the erosive action of the high cost of living, it is necessary to know how to value one's savings over time and to exploit the tools of private banking.

How can this be done?

This is the task of good private bankers, who must make their clients understand how harmful the choice of leaving their wealth parked in liquidity without returns is.

Historically, various asset classes have managed to ensure in the medium and long term a capital appreciation higher than inflation, protecting it from the erosive action of the price increase.

Fonte Banca Generali

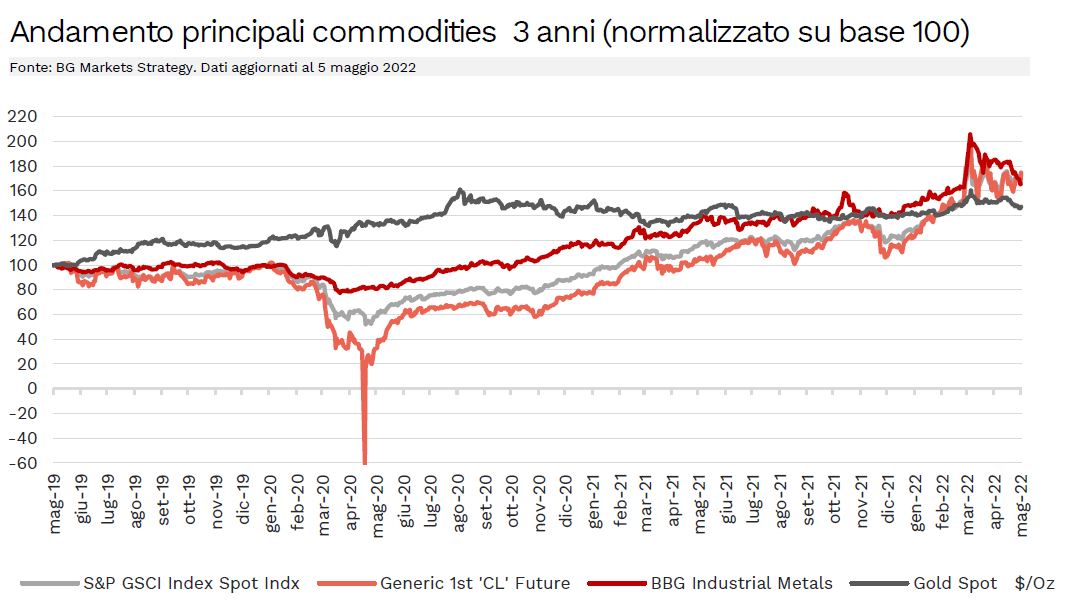

This is the case of shares which can be volatile in prices in the short term but which, in the medium and long term, have always performed well above the cost of living. The so-called real assets, such as raw materials, should not be forgotten.

When an inflationary flare-up is triggered by commodities as has happened in recent months, it is obvious that those with portfolio exposure to the commodities sector can defend themselves against the effects of rising cost of living. The same consideration applies to another category of real assets such as real estate and to gold: the precious metal traditionally considered a safe haven which, beyond short-term fluctuations, has retained value over time, protecting investors from devaluation.

Of course, focusing on a single asset class is always counterproductive. Inflation risk, like all risks, must also be faced with a walletwell diversified, built thanks to the expertise of a good financial advisor.

Given these premises, one thing is clear: those who want to defend their wealth from the erosive action of high prices, today cannot stand at the window, parking it in liquidity.

Inflation, in the economic sector, is a very important indicator as it shows a growth in prices over time that consequently determines a decrease in the purchasing power of money.