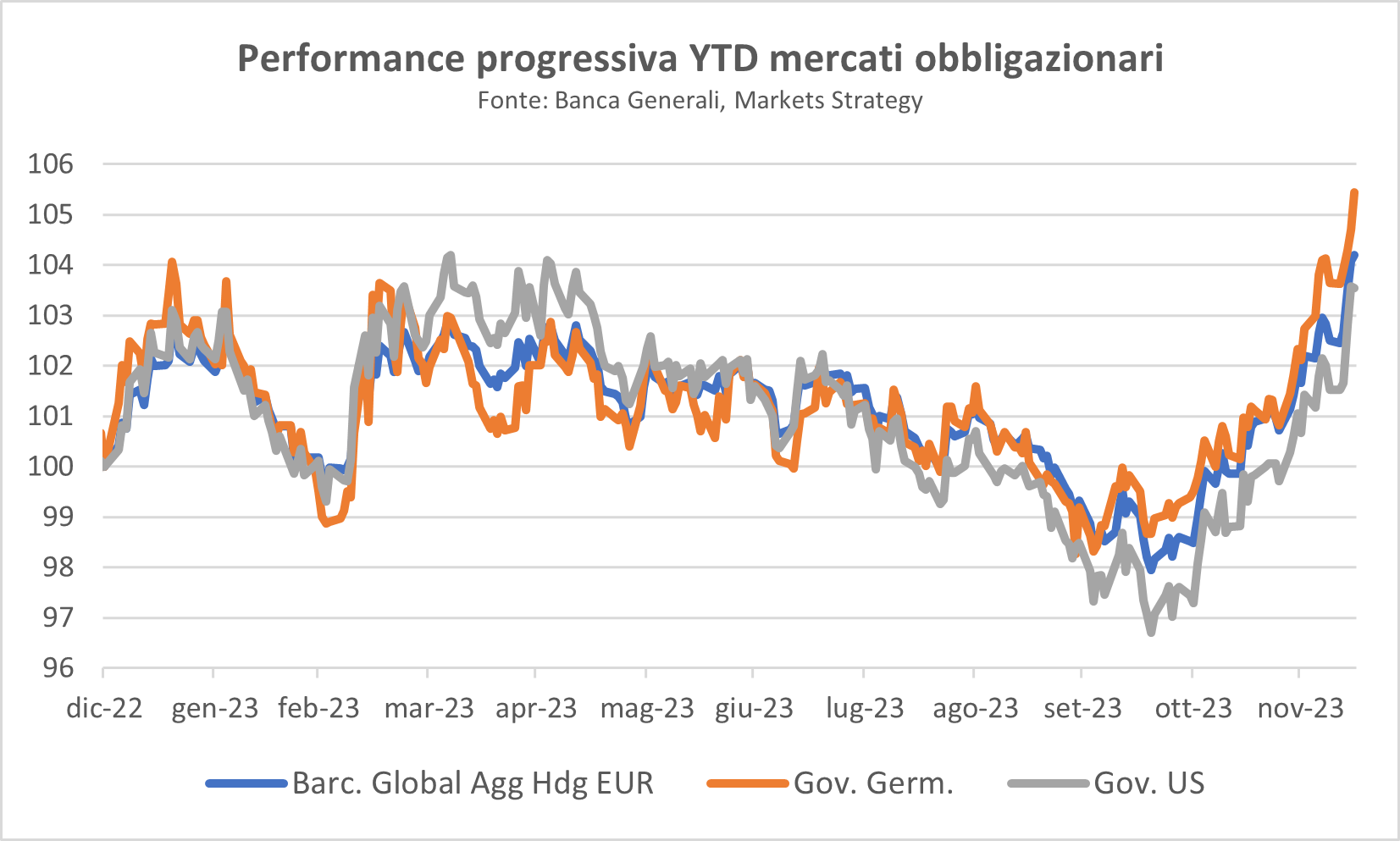

"Much of the upward movement in both stock and bond prices occurred in the latter part of the year, thanks to the growing belief among traders that central banks were now close to defeating the inflationary dynamic that has characterized the world economy since 2021," comments Generoso Perrotta, head of Financial Advisory at Banca Generali.

Supporting this hypothesis were inflation data in both the United States and the Eurozone. Indeed, consumer price growth in the U.S. fell to 3.1 percent in November 2023 from its peak of 9.1 percent in June 2022, while in the Eurozone, in the same month, it rose to 2.4 percent from its peak of 10.6 percent in October 2022.

"Such evidence has led, in recent months, to sharply revised forecasts of future central bank moves in favor of sharp interest rate cuts in both macro areas (the U.S. and Europe). Similar outlooks, in favor of a benign soft landing of developed economies, have pushed up stock markets, sharply declining core yields (rising bond prices) and sharply narrowing corporate spreads," the expert further comments.

Despite a positive environment for equity markets, the performance of the major international indices has been characterized by pronounced variability.

Generoso Perrotta, Head of Financial Advisory at Banca Generali

Generoso Perrotta, Head of Financial Advisory at Banca Generali