Of course, these are "rough" calculations, but they give an idea of how the rising cost of money affects the budget of indebted households. However, one important detail should not be forgotten.

In addition to fixed-rate or variable-rate mortgages, there are other "hybrid" types of financing on the market: this is the case with mixed-rate mortgages, which allow you to switch from fixed-rate to variable-rate at certain maturities, or mortgages with a cap, which have an indexed interest amortization schedule, for which, however, there is a ceiling, beyond which they cannot go.

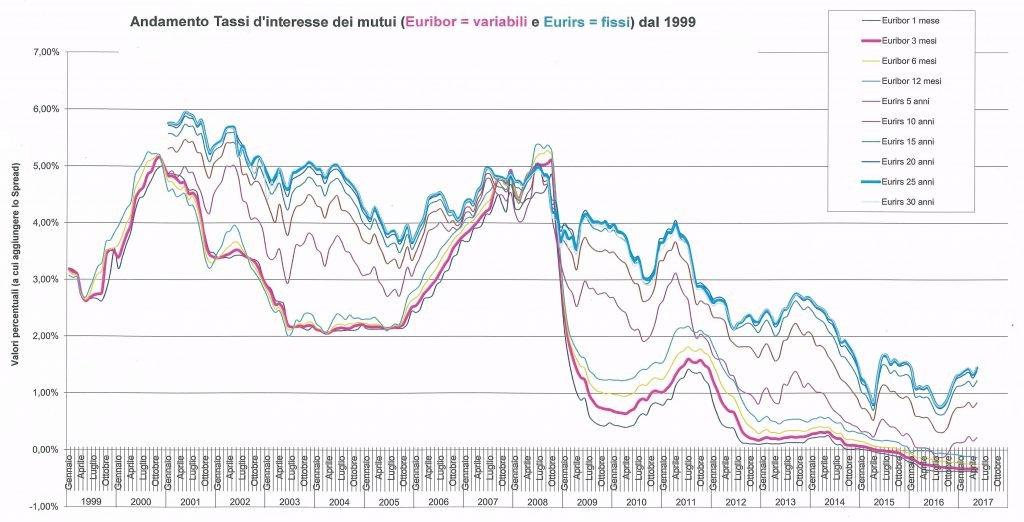

The considerations made so far apply to those who have already gone into debt to buy property in the past months or years. Different discussion for those who, on the other hand, have yet to take out a new mortgage and are faced with the starting dilemma: better fixed rate or variable rate?

In this case, those who want to sleep soundly and know in advance what installment they will pay until the end of the repayment plan can only choose a fixed-rate mortgage. However, there is also the other side of the coin: variable-rate mortgages, being riskier because they have installments that vary over time, usually cost less than fixed-interest mortgages (obviously with the same maturity and amount of debt), that is, they have a lower starting rate and installment.

To realize this, just consider the concrete example of a 200-thousand-euro mortgage with a 25-year maturity, intended for the purchase of a property worth 250 thousand euros. In this case, those who choose the variable-rate solution pay a monthly installment of about 780-800 euros. On the other hand, those who opt for the security of the fixed rate must shell out an amount of 950-1,000 euros each month, or 200 euros more.

Sleeping soundly, in short, is not cost-free.

Paolo Baldessari, Head of Fixed Income & Alternative Investments at Banca Generali

Paolo Baldessari, Head of Fixed Income & Alternative Investments at Banca Generali